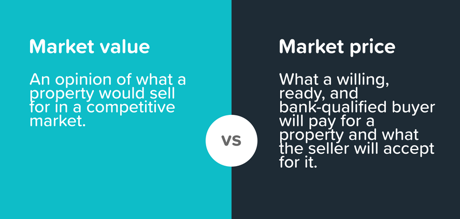

The market price of your is based on what willing buyers in the market will pay for your home. However, buyers are all different with different needs, wants, tastes. For some buyers, location is paramount. Families may consider schools over the size and condition of a home.

The market price of your is based on what willing buyers in the market will pay for your home. However, buyers are all different with different needs, wants, tastes. For some buyers, location is paramount. Families may consider schools over the size and condition of a home.

The market value is an opinion of what a property would sell for in a competitive market based on the features and benefits of that property (the value), the overall real estate market, supply and demand, and what other similar properties have sold for in the same condition.

So as you can see, while each valuation model is similar, there is a difference. Market value is determined by the overall dynamics of the market. Market price is determined by buyers' choices.

We’ve outlined some of the most important factors that influence your home’s value:

1. Neighborhood comparables

The main indicators of your home’s value are the sold prices of similar homes in your neighborhood that have sold recently. These homes are referred to as “comps”. Whether it’s a home appraisal, a comparative market analysis done by an agent, real estate experts will rely on comps to estimate your home value. Generally:

- Recency: Homes that were recently sold— six months (if available), one year if scant comps.

- Feature Similarity:Homes that are most similar to yours: type of home (two-story vs. ranch), year built, number of bedrooms, bathrooms, square footage, lot size, garage/no garage.

- Distance: If possible, homes in the same subdivision as your home. This is because the house a block over may not be a good comparable if it belongs to a different subdivision with different HOA rules, school district, etc. If more rural, physical distance; i.e., within 5 miles, 10 miles in like areas.

- Location: Corner lot, quiet cul-de-sac, busy street, golf course, waterfront, distance to goods/services, etc.

The challenge is that no two comps are the same so your real estate expert should make $$ adjustments for key differences. Granular details like vaulted ceilings, proximity to a good school, or abstracts like panoramic view are marginally considered. Overall, the main characteristics of the subject property vs. comps are utilized to arrive at market value. In general, and if available, approximately 3-5 comparables will be utilized.

2. Location

Your current home may be the ideal location for you. Maybe close to your job, medical services, shopping, restaurants. But when real estate experts determine how much value to assign based on the location of the house, they’re looking at three primary indicators: The quality of local schools, employment opportunities, proximity to shopping, entertainment, and recreational centers. When it comes to calculating a home’s value, location can be more important than even the size and condition of the house.

3. Home size and livable space

When estimating your home’s market value, size is an important element to consider, since a bigger home can positively impact its valuation. The value of a home is roughly estimated in price per square foot after adjustments are made to the comps. That is the comps' aggregate sales prices divided by the square footage of the home. In addition to square footage, a home’s usable space is extremely important when determining its value. Garages, attics, and unfinished basements, Arizona rooms, unheated areas, are generally not counted in usable square footage. Livable space is what is most important to buyers and appraisers. Bedrooms and bathrooms are most highly valued, so the more beds and baths your home offers, the more your home is generally worth.

4. Age and condition

Typically, homes that are newer appraise at a higher value. The fact that critical parts of the house, like plumbing, electrical, the roof, and appliances are newer and therefore less likely to break down, can generate savings for a buyer. For example, if a roof has a 20-year warranty, that’s money an owner will save over the next two decades, compared to an older home that may need a roof replaced in just a few years. Many buyers will pay top-dollar for a move-in-ready home. This is why buyers should require a Home Inspection in their contract — to negotiate repairs and/or to avoid any major expenses following the sale. This home maintenance and repair checklist can help identify items of your home to take a look at before listing.

5. Upgrades and updates

Updates and upgrades can add value to your home, especially in older homes that may have outdated features. However, not all home improvement projects are created equally. The financial rewards or benefits of a project or upgrade varies based on the market you’re in, and you’re existing home value. Check out suggested improvement values with this home improvement value calculator. Some projects like adding a pool or wood floors tend to have bigger increases for more expensive homes, while projects like a kitchen remodel or adding a full bathroom tend to have a bigger increase for less expensive homes.

6. Market influences

Even if your home is in great condition, located in the best area, with premium upgrades, the number of other homes for sale in your area and the number of buyers in the market can impact your home value. Lot of buyers competing for fewer homes it’s a seller’s market. Fewer buyers but many homes on the market is a buyer’s market. In a buyer’s market, buyers have more room to negotiate the home’s price, timeline, and contingencies in the contract. If you’re selling in a buyer’s market, you may have to consider adjusting the price to attract more offers. You may consider making concessions as a seller, like paying some closing costs, covering repairs, or being more flexible with the timeline. Market conditions can affect how long it takes your home to sell. In a seller’s market, homes tend to sell quickly. In a buyer’s market it’s typical for homes to see longer days on market (DOM) which is a market statistic that indicates how long homes are actively listed before a contract is signed. If your home has been on the market for a longer period of time, buyers may perceive there is something wrong or that the price is too high.

for sale in your area and the number of buyers in the market can impact your home value. Lot of buyers competing for fewer homes it’s a seller’s market. Fewer buyers but many homes on the market is a buyer’s market. In a buyer’s market, buyers have more room to negotiate the home’s price, timeline, and contingencies in the contract. If you’re selling in a buyer’s market, you may have to consider adjusting the price to attract more offers. You may consider making concessions as a seller, like paying some closing costs, covering repairs, or being more flexible with the timeline. Market conditions can affect how long it takes your home to sell. In a seller’s market, homes tend to sell quickly. In a buyer’s market it’s typical for homes to see longer days on market (DOM) which is a market statistic that indicates how long homes are actively listed before a contract is signed. If your home has been on the market for a longer period of time, buyers may perceive there is something wrong or that the price is too high.

7. Economic conditions

The broader economy often impacts a person’s ability to buy or sell a home. In slower economic conditions, the housing market can struggle if employment or wage growth slows, then fewer people might be able to afford a home or there may also be less opportunity to relocate for new employment opportunities. It’s important to keep up with the current status of home sales and home price appreciation in your area, especially when as you evaluate the best time to sell your house.

8. Interest rates

Both short-term interest rates and long-term interest rates affect your ability to afford a home, but in different ways. An increase in short-term interest rates might increase the interest paid on your savings, but it also makes short-term debt more expensive. For example, if you’re spending more money paying off a credit card or short-term loan, then you will likely have less money available in your budget to afford a home. Short-term interest rates typically don’t affect long term interest rates. An increase in the Federal Funds rate, doesn’t mean a 30-year, fixed-rate mortgage will become more expensive. Long-term rates are influenced by Department of the Treasury yields, investor sentiment, and inflation rates, among many other factors. As interest rates increase, less people may be able to afford to buy homes. This factor can impact how much you can sell your home for.

Both short-term interest rates and long-term interest rates affect your ability to afford a home, but in different ways. An increase in short-term interest rates might increase the interest paid on your savings, but it also makes short-term debt more expensive. For example, if you’re spending more money paying off a credit card or short-term loan, then you will likely have less money available in your budget to afford a home. Short-term interest rates typically don’t affect long term interest rates. An increase in the Federal Funds rate, doesn’t mean a 30-year, fixed-rate mortgage will become more expensive. Long-term rates are influenced by Department of the Treasury yields, investor sentiment, and inflation rates, among many other factors. As interest rates increase, less people may be able to afford to buy homes. This factor can impact how much you can sell your home for.